Dashboard: Dashboard · method: _RESEARCH-METHOD · market grid: _MARKET-PROBLEM-MAP · opportunity lens: _OPPORTUNITY-LENS · landscape: competitor-landscape-report

Purpose: this brief is different from the others in the set. It does not ask “can we beat Procore” — the honest answer is no, not head-on. It exists to answer two questions that govern every other dossier: (a) how real is Procore’s shipped AI today versus the slideware, and (b) would Procore bundle our commercial / claims-AI wedge for free into the system of record before we can establish a foothold. The brief first explains what Procore is and why it is entrenched, then maps its surface, then lands on the read that matters: Procore is the platform we plan around, not the one we attack. Evidence (a 100-review segmentation sample, App Store data, vendor product/pricing/AI/developer pages, video walkthroughs) is at the end.

Snapshot

| What it is | The construction system of record — a single cloud platform holding a project’s drawings, RFIs, submittals, daily logs, budgets, contracts, change orders and field data, used by owners, general contractors and specialty contractors together |

| Core job it does | Becomes the one place every party on a project works, so the project’s data, money and documents live in one auditable system instead of email and spreadsheets |

| Who buys | Mid-market to enterprise GCs, large specialty subs, and owners/developers; reportedly targeted at firms with ~$20M+ annual construction volume; ~2M users across 150+ countries (US-centred, global reach) |

| Business model | Sales-led, enterprise, annual contract priced on Annual Construction Volume (ACV) — a slice of the dollar value of work run through it — not per-seat; unlimited users included; long implementations |

| Openness | Public REST API (OAuth2), webhooks, developer sandbox, and an App Marketplace of 200+ (vendor says 500+) integrations; developers can now register MCP servers and AI agents as app components |

| Public ratings | App Store 4.65 (44,281 ratings, US) / 4.60 (1,052, GB); Capterra ~4.5 (~2,645 reviews); G2 4.6 (4,094) |

| Strongest areas | Project management as system of record; RFIs/submittals/document control; cost & financials; field/daily reporting; quality & safety |

| Weakest areas (our interest) | Change/variation/claims/entitlement recovery as a workflow; historical-cost benchmarking across firms; estimating/takeoff (acquired, thinner) |

| Our verdict | Do not fight head-on. Procore owns distribution and is shipping real AI fast; it is the walk-away risk for our other plays, not a target |

Where Procore plays across the market

Scored 0 (not addressed) to 100 (best-in-class) against the 21 areas in _MARKET-PROBLEM-MAP, sorted by coverage. Procore is the broadest product in the set, so most areas score high; the few that do not are the interesting ones.

| Problem area | Coverage | Note |

|---|---|---|

| Project Management (system of record) | 100 | The product. The central source of truth every other module hangs off |

| RFIs / Submittals / Document Control | 95 | Best-in-class: drawings, spec versions, RFI/submittal logs with cost/schedule impact flags |

| Cost Management & Forecasting | 90 | Budgets, commitments, change events, forecasting, owner/prime contracts, invoice management |

| Communication & Client Collaboration | 90 | Unlimited users (incl. owners and subs); Conversations (open beta); the whole platform is a shared workspace |

| Field Mgmt / Daily Reporting | 85 | Daily logs, photos, punch list, drawings, documents in the field; voice “Quick Capture” |

| Quality / QA-QC / Snagging | 85 | Observations, inspections, incidents, punch list |

| Safety & Compliance | 80 | Incidents, inspections, observations, safety analytics; photo-based safety insights via AI |

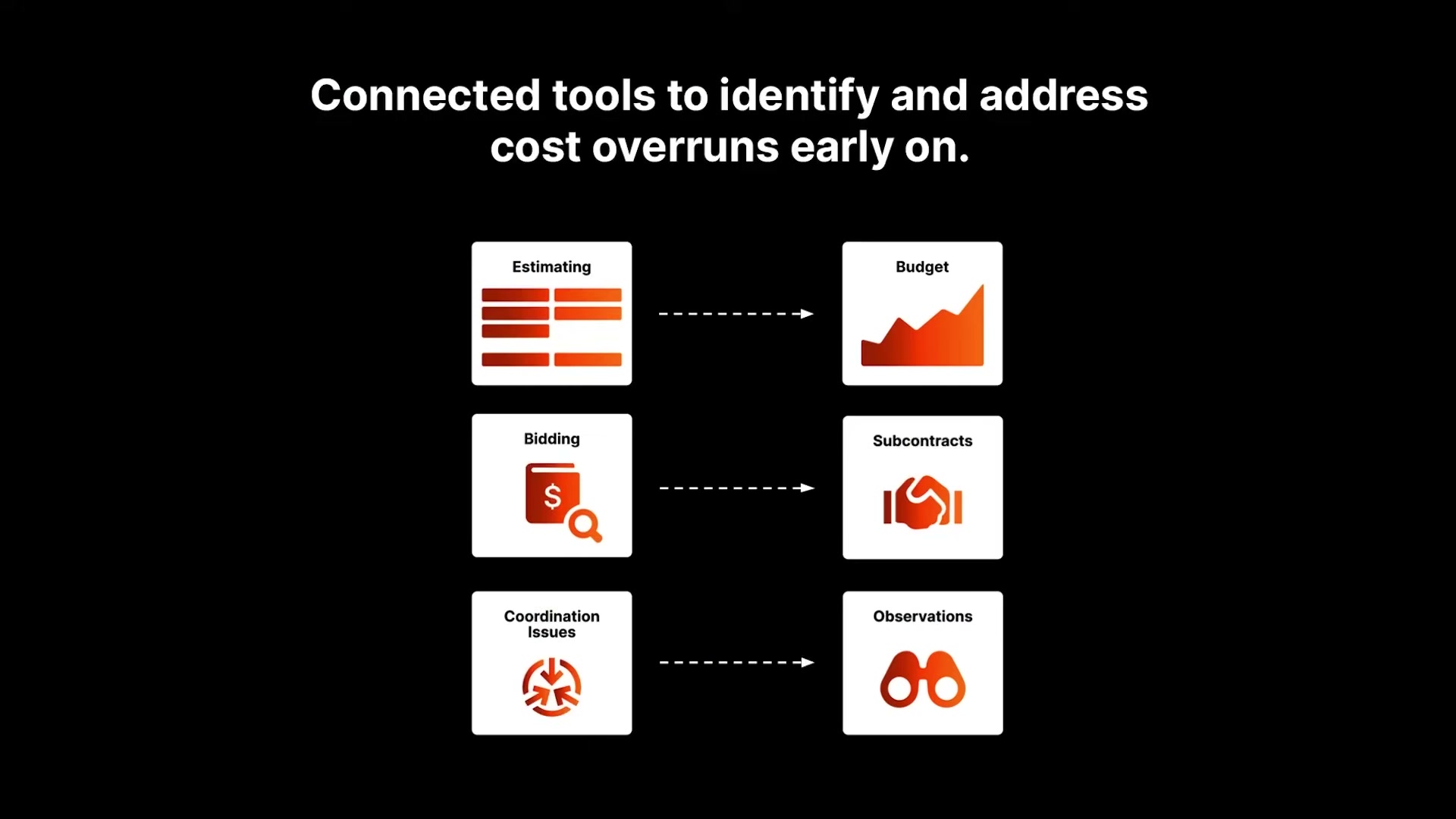

| Change / Variations / Claims / Entitlement | 70 | Strong on change orders / change events as commercial records; weaker on claims/entitlement recovery as a narrative-and-evidence workflow |

| BIM / Design Coordination | 75 | BIM coordination, model viewing, coordination issues tied to the record |

| Insurance & Risk | 70 | Insights/risk benchmarking, compliance tracking; Contract Review agent flags risk |

| Time, Labour & Workforce | 70 | Workforce/Resource Management, timecards, timesheets, T&M tickets (Field Productivity priced separately) |

| Progress & Production Tracking | 70 | Actual-vs-plan via Resource Management, 360 Reporting, Analytics 2.0 |

| Scheduling / Programme | 65 | Schedule tool plus deep integrations to P6/MS Project; not its own scheduling engine |

| Bid & Tender Management | 65 | Bid Management module; BuildingConnected sits adjacent in the Procore orbit |

| Accounting / AP-AR / Payroll | 60 | Invoice management and a money-in/money-out layer, but the ledger lives in the ERP integration (Sage/Viewpoint/QuickBooks) |

| Prequalification & Procurement | 60 | Commitments, POs, prequalification; procurement workflows |

| Reality Capture / Drone / Survey | 55 | Photos/360; reality capture mainly via marketplace (DroneDeploy, EarthCam) |

| Equipment / Asset / Material Tracking | 55 | Resource Management covers equipment/materials planning; not a fleet-telematics product |

| O&M / Handover / Golden Thread | 50 | Closeout and the as-built record exist; handover is a by-product of the record, not a dedicated module |

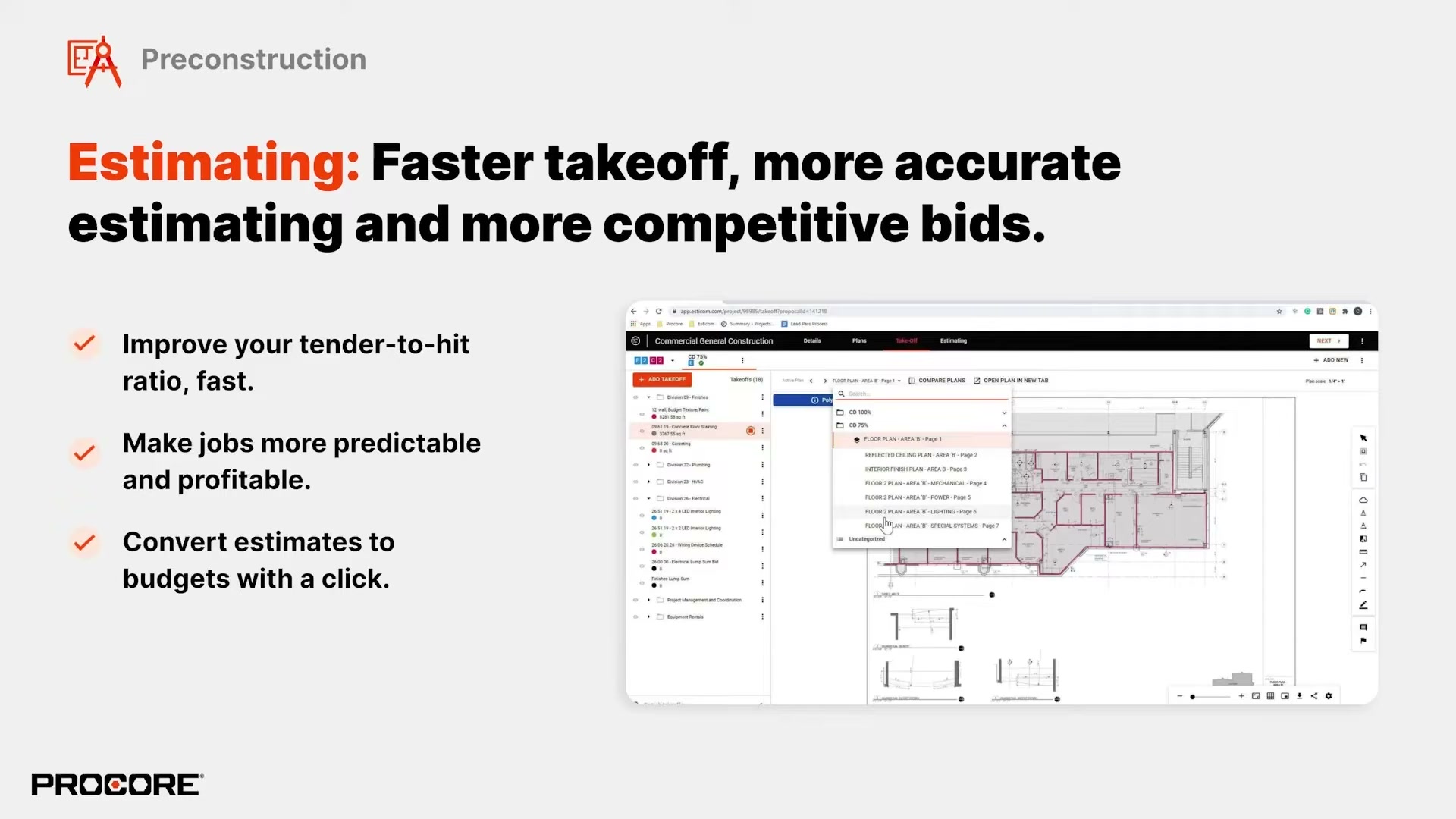

| Estimating & Takeoff | 45 | Procore Estimating exists (built on an acquisition) but is thinner than specialist takeoff tools |

| Historical Cost / Benchmarking Intelligence | 55 | Insights benchmarks KPIs vs industry; cross-project/cross-firm cost benchmarking is emerging, not a mature product |

Takeaway: Procore is wide and deep across the centre of the market — the system of record, documents, cost and field. The two areas central to our own thesis are the only relative softness: claims/entitlement as a money-recovery workflow (Procore records changes well but does not run the narrative-building-and-recovery process), and historical-cost benchmarking (data exists; the cross-firm benchmarking product is early). But “relative softness” here means “a 55-70 inside a platform everyone already pays for,” which is a very different proposition from the gaps we found in narrower tools.

The input side — how work gets captured

- Captured: drawings and spec sets, RFIs, submittals, daily logs, photos and video, punch list items, observations, inspections, incidents, timecards and timesheets, T&M tickets, change events, commitments, and contract documents — across owner, GC and sub.

- Input methods: mobile apps (iOS/iPad/Android) for the field; web for the office; voice “Quick Capture” that turns a narrated job-site video into a structured punch item; bookmarks for fast item access; offline-capable drawings.

- Onboarding / ease: the recurring user complaint is the opposite of the small-tool story — Procore is powerful but has a steep learning curve and heavy configuration. It is a platform you implement, not an app you download. Implementation services are bundled into the contract precisely because it needs them.

- Friction (from reviews and the sample): complexity and the learning curve; the cost; configuration effort. The capture itself is comprehensive; the friction is breadth and price, not missing function.

The management side — what the office sees

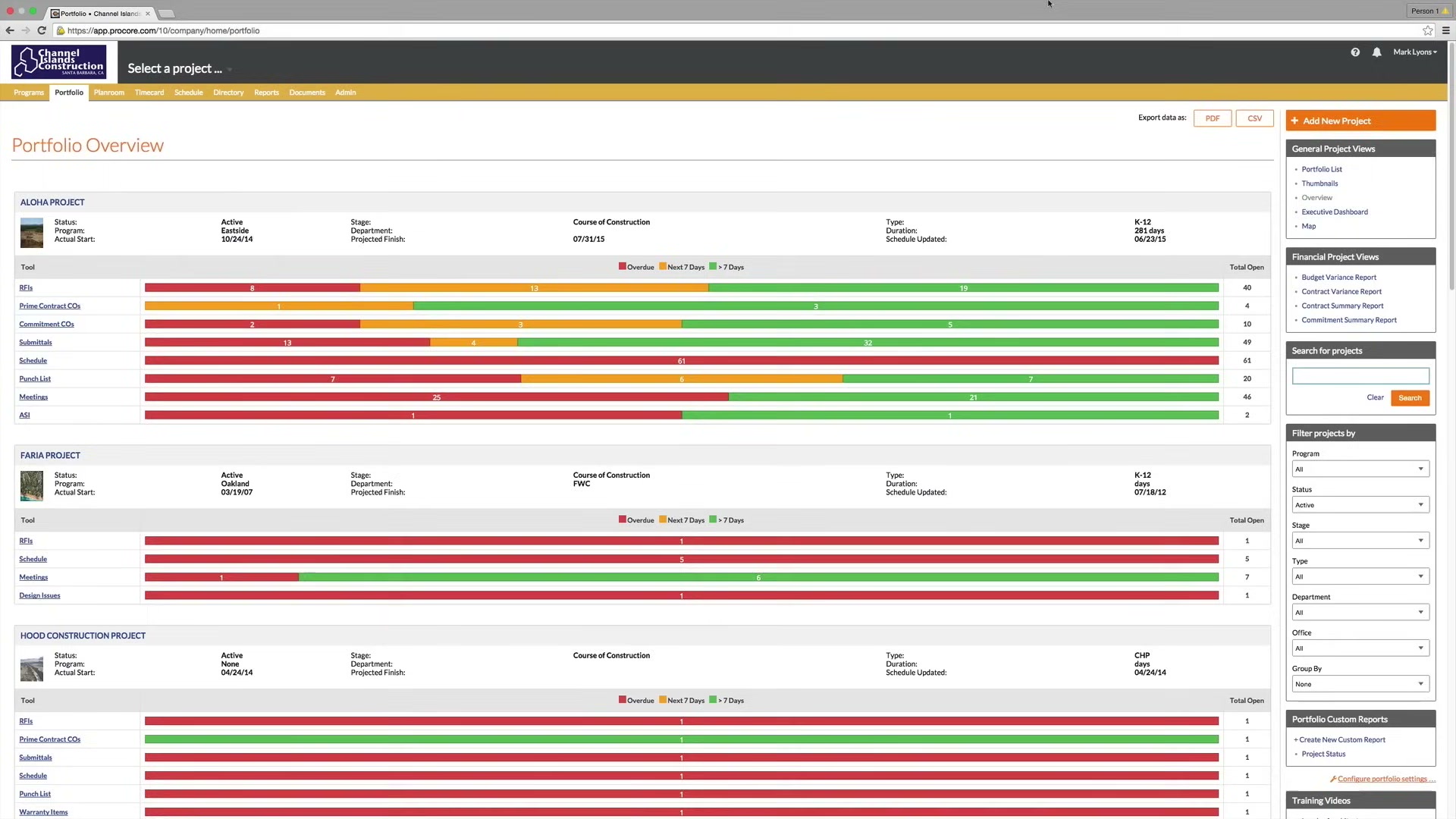

- Lands in the web platform: a Portfolio Overview across all projects (RFI/submittal/punch/financial status as red-amber-green bars), per-project dashboards, open-RFI logs with cost-impact and schedule-impact columns, budget and forecast views, change-event and commitment ledgers, 360 Reporting and Analytics 2.0, and Insights risk/KPI benchmarking.

- Who consumes: project managers and project engineers (RFIs, submittals, drawings), project controls and finance (budget, commitments, change, forecast, invoices), executives (portfolio-level risk and status), and — uniquely — owners and subcontractors inside the same system, because users are unlimited.

- Valued most: one auditable source of truth; document control; the fact that everyone on the project works in the same place.

- Pains: breadth and learning curve; cost; configuration; some modules (estimating, scheduling) less loved than the core.

- Structural point (not a gap to exploit, a moat to respect): unlike the operational-only dashboards in narrower tools, Procore’s office side already spans documents, cost, change and risk together. The data loop — every party entering the project’s data into one system that the money and the audit trail run through — is the strongest moat in the competitor set. It is not a seam we can slip into; it is the thing that makes Procore the default.

Where the value actually comes from

| Sales story (what wins the deal) | Real source of stickiness (what makes it impossible to leave) |

|---|---|

| One platform for the whole project; unlimited users; visibility from preconstruction to closeout | The project’s entire record — drawings, RFIs, contracts, change orders, financials — lives here and is wired into the firm’s ERP and 200+ other tools; every party (owner, GC, sub) is already inside it; leaving means re-platforming the system of record mid-portfolio |

- Do not attack: the system of record itself, document control, the cost/financials core, the unlimited-user collaboration model, the ERP and marketplace integrations, the owner-GC-sub network effect. This is Procore’s home ground and it is genuinely best-in-class.

- Where value stops (and even here, carefully): Procore records a change order as a commercial document; it does not run the entitlement-recovery workflow — assembling the delay/disruption narrative, marshalling the photographic and log evidence into a defensible claim, drafting the claim itself. And cross-firm historical-cost benchmarking is early. These are the only places the platform’s value thins — but they thin inside a system the customer already owns, which is exactly why they are dangerous to build a business against (see Our read).

What users say — both sides

Credibility first: this is a 100-review segmentation sample drawn from Procore’s ~2,645 total Capterra reviews — a four-page slice, not full coverage; treat the shares as indicative, not population-accurate. Within the sample, zero reviews were flagged vendor-solicited, 48% are explicitly organic (no incentive) and 52% carried a nominal gift — a healthier organic mix than the heavily-solicited corpora seen on smaller tools. The headline number to watch is the same one that recurs across the market: even with blank entries excluded, the weakest sub-rating is value for money at 4.07, the lowest of the four despite Procore’s otherwise strong scores (features 4.58, support 4.44, ease 4.39). Procore users rate price-to-value below everything else they score.

| Praised | Criticised |

|---|---|

| One central source of truth; document control | Cost / value for money (lowest sub-rating, 4.07) |

| Everyone (owner, GC, sub) works in one system | Steep learning curve; heavy configuration |

| RFI / submittal / drawing management | Breadth can overwhelm smaller teams |

| Real-time field-to-office visibility | Some modules (estimating, scheduling) weaker than the core |

| Strong integrations and reporting | Occasional mobile app reliability complaints |

- Signal for us: the price grievance is real and universal even here — but it is not a wedge against Procore, because the cost buys breadth no point tool matches. The more useful signal is the absence of a strong “missing change orders / can’t build a claim” complaint: Procore’s users do not feel the commercial-recovery gap acutely, because the platform records changes competently. That tells us the claims-recovery opportunity lives with the narrower tools’ users, not Procore’s.

The opportunity for AI in this space

- The job here is highly LLM-shaped — which is exactly why Procore is doing it themselves. RFI drafting, submittal review against specs, daily-log synthesis from photos and voice, contract-risk review, deep document search — these are the textbook cheap-AI tasks. In most dossiers that observation is our opening. Here it is the warning: the document-heavy generative layer that we would build on a narrower tool’s data is the layer Procore has already shipped agents for, on top of the richest construction dataset in the market.

- Where cheap AI still cannot eat Procore’s job: nothing structural protects the task from AI; what protects Procore is data access and distribution. The agents only work because the RFIs, specs, drawings and contracts are already in Procore. An outside AI layer cannot get that data without Procore’s permission, and Procore has no reason to grant it for the commercial layer it can serve itself.

What this means for what we would build:

- Do not build an AI layer that competes with Procore agents on Procore’s data. It is the one place the “inference is free, so we win the generative layer” logic fails — because the data is not free to reach and the distribution-owner is already there.

- Build where Procore’s data loop does not reach: firms and projects not on Procore (the long tail of mid-market and UK/EU contractors Procore’s $20M-volume, US-centred motion under-serves), and the cross-firm historical-cost benchmarking layer that no single platform — Procore included — owns yet, because it requires data across competitors’ walled gardens.

How open the platform is

- API / integrations: public REST API (OAuth2), webhooks / change notifications, a per-app developer sandbox with seeded data (cost codes, RFIs, submittals, drawings), transparent rate limits, SOC 2 Type II, SSO. The App Marketplace carries 200+ integrations (Procore markets “500+”) across ~25 categories — ERP/accounting (Sage, Viewpoint/Vista, QuickBooks), BIM (Autodesk, Bluebeam), drone/reality capture (DroneDeploy, EarthCam), and more; Procore says 95%+ of customers run at least one integration.

- What the openness means — and the trap inside it: the API is genuinely open, which normally favours a build-on-top entrant. But Procore has now opened the developer platform to let partners register MCP servers and AI agents as components of a Procore app. Read carefully, that is the opposite of an opening: it invites third-party AI to run inside Procore’s distribution and governance, on Procore’s terms, deepening the platform rather than letting an independent AI layer sit outside it. Building on Procore’s API makes you a marketplace tenant, not an independent business — and the landlord is shipping the same agents you would.

Procore’s own AI — claims, shipping, and how far they can go

Procore is the one competitor in the set where the talk-versus-ship gap is narrow. It announced its AI direction at Groundbreak 2024, named the architecture (Helix) and an assistant and agents in 2025, then bought an agentic-AI company (Datagrid, closed Jan 20 2026) and shipped a suite of working agents on May 21 2026. This is not slideware.

| Feature | What it does | Status | Date |

|---|---|---|---|

| Procore Helix | The intelligence layer / AI foundation the rest is built on | GA (announced as the foundation) | Groundbreak 2025 |

| Procore Assist (formerly Copilot) | Conversational assistant; cited answers from specs/RFIs/submittals/codes; photo intelligence; multilingual (Spanish/Polish); mobile | GA, with enhancements | Groundbreak 2025 |

| Procore Agent Builder | No-code builder for custom agents from natural-language prompts | Open beta (all customers) | Groundbreak 2025 |

| Datagrid acquisition | Built-environment agentic-AI platform; 90+ data connectors; reasoning engine; Agent Builder | Acquisition closed | 20 Jan 2026 |

| RFI Agent | Checks RFIs for completeness/clarity; suggests edits; attaches docs | Beta (Datagrid-in-Procore private beta) | 21 May 2026 |

| Submittal Reviewer Agent | Reviews submittals against specs; flags discrepancies | Beta | 21 May 2026 |

| Deep Search Agent | Searches specs/drawings/RFIs; consolidates references; highlights conflicts; links to source | Beta | 21 May 2026 |

| Daily Log Agent | Aggregates photos/emails/voice notes into a draft daily log | Beta | 21 May 2026 |

| Contract Review Agent | Flags contract conflicts and risks; comments in contracts/drawings | Beta | 21 May 2026 |

| Actions & Triggers | Lets agents execute tasks in Procore and respond to project events automatically | Beta | 21 May 2026 |

- The native Datagrid-in-Procore experience is in private beta with paid general availability promised “beginning this summer” (2026); the standalone Datagrid Pro/Enterprise offerings are already purchasable today. So the precise read is: the platform AI assistant (Assist) and the agent builder are GA; the deep workflow agents are real, demoed and in beta, days old, going GA imminently.

- Crucially, the shipped/beta agents already cover the document-heavy layer — RFIs, submittals, daily logs, contract review, deep search — that is exactly where an outside claims/commercial-AI wedge would aim. Procore is building toward the commercial layer from inside the system of record, with the data and the distribution we would lack.

- Confidence Procore closes the commercial-AI gap on its own turf within ~2 years: high (about 3 in 4). Reasons: it has the data, the distribution, a working agent platform, a no-code builder, and now an acquired AI team; the cadence (announce 2024 → architecture 2025 → acquire + ship 2026) is fast for an incumbent; and Actions/Triggers show it intends agents that do work, not just summarise. The main thing it does not yet have is a dedicated entitlement-recovery / claims product and a cross-firm benchmarking product — but those are adjacent, not distant, for a company on this trajectory. This is the read that makes Procore the walk-away risk for our other dossiers.

Who actually uses Procore

From the 100-review segmentation sample (a four-page slice of ~2,645 Capterra reviews — indicative, not population-accurate):

| Company size | Share (sample) | Avg overall |

|---|---|---|

| 1-10 employees | 18% | 4.0★ |

| 11-50 employees | 30% | 4.5★ |

| 51-200 employees | 37% | 4.54★ |

| 501-1,000 employees | 6% | 5.0★ |

| 1,001-5,000 employees | 2% | 4.0★ |

| 5,001-10,000 employees | 2% | 4.5★ |

| 10,001+ employees | 2% | 4.5★ |

- The Capterra sample skews to smaller firms (reviewers self-select), but the real Procore buyer is mid-market-to-enterprise — the vendor’s own positioning targets firms with ~$20M+ annual construction volume, and the platform is built for owner-GC-sub collaboration at scale. Satisfaction is high and flat across sizes; the constraint on small firms is price and complexity, not fit.

- Role: office 59% vs field 5% in the sample (the rest mixed) — the paying decision and the heavy usage sit firmly in the office.

- Industry: overwhelmingly construction (68 of 100), then architecture & planning, commercial real estate.

- Alternatives considered (sample): the names that appear are tellingly Procore-orbit and specialist — Autodesk (Forma/Construction Cloud), Bluebeam, STACK, BuildingConnected, ConstructConnect, Oracle Textura, GCPay — i.e. people shopping Procore are comparing it to other platforms and serious point tools, not cheap apps.

- Switched from: Sage Construction Suite, Excel, Fieldwire, Buildertrend, monday.com, Jobpac — a mix of ERPs, spreadsheets and lighter PM tools that Procore consolidates.

Our read — can we enter and win?

Not against Procore, and the discipline of this brief is to say so plainly. Procore is the distribution-owner: it holds the construction system of record, prices on construction volume rather than seats (so it has no per-seat revenue to cannibalise by giving AI away), bundles unlimited users, runs the strongest data-and-network moat in the set, and — decisively — is shipping real agentic AI fast, having just bought the team to do it. The classic entrant logic (“software is free to build, inference is free, so we wrap the incumbent’s data in an AI layer and flank the commercial gap”) is precisely the logic that fails here, because the data is inside Procore’s walls and Procore is already building the agents. Anything we built on Procore’s API would be a marketplace tenant on the landlord’s terms, competing with the landlord’s own agents.

So Procore is not a target — it is the constraint we design around. Two practical conclusions for the rest of the programme. First, the commercial/claims-AI and historical-cost wedges we like are only safe where Procore’s data loop does not reach: firms and geographies it under-serves (UK/EU mid-market commercial and fit-out contractors; sub-$20M-volume firms; projects not run on Procore), and the cross-firm benchmarking layer that no single platform can own because it needs data across competitors’ walled gardens. Second, Procore is the walk-away test for our other dossiers: if a wedge we are considering sits on data a Procore-class platform already holds, and Procore could ship it as a free agent, we do not enter. The honest verdict is to flank into the spaces Procore’s distribution does not cover, and never to meet it head-on.

| Question | Our read |

|---|---|

| Where is Procore strong and off-limits? | The system of record, document control, cost/financials, owner-GC-sub collaboration, ERP + marketplace integrations, and now shipped agentic AI — essentially the whole centre of the market |

| Where is the verified relative softness? | Entitlement/claims-recovery as a workflow (it records changes, doesn’t run recovery) and cross-firm historical-cost benchmarking — but both sit inside a platform the customer already owns |

| How hard for Procore to follow us into those? | Easy and likely. It has the data, distribution, a working agent platform and a no-code builder; confidence it closes the commercial-AI gap on its own turf in ~2 years is high (~3 in 4) |

| How much can cheap AI do here? | A great deal — and that is the problem, because Procore is already doing it on the data we could not reach |

| Is there a cheap, narrow way in against Procore? | No. Building on its API makes us a tenant; its pricing model leaves no per-seat revenue to undercut; it bundles AI for free |

| What would make us walk away (this is the test for other dossiers)? | A Procore-class distribution-owner bundling the same wedge as a free agent on data it already holds — which is exactly Procore’s trajectory |

| Overall | Avoid head-on. Treat Procore as the platform to plan around and the walk-away risk for the whole programme; flank only into spaces its distribution does not cover |

The app itself — ratings and reception

| Store | Rating | Ratings count | Version |

|---|---|---|---|

| App Store (US) | 4.65 | 44,281 | 2026.0603 |

| App Store (GB) | 4.60 | 1,052 | 2026.0603 |

| Capterra | ~4.5 | ~2,645 | — (100-review sample analysed) |

| G2 | 4.6 | 4,094 | — |

The mobile app is the field front door to a platform whose centre of gravity is the web. The 44k US rating count is an order of magnitude above the narrower tools in the set and reflects Procore’s reach — ~2M users, 150+ countries. The listing leads on field enablement (drawings, daily log, punch list, RFIs, photos), workforce management (timecards/timesheets/T&M), project management, quality & safety, and project financials — the platform’s breadth, condensed.

Screenshots

Grouped by theme, full-size and scrollable. Images render in Obsidian and exported HTML through embeds (referenced, not copied). The App Store listing exposes no marketing screenshots via the API (screens count 0), so the visual pack here is built almost entirely from walkthrough-video frames showing real product UI — which is the more valuable side anyway, since Procore’s value lives in the web office surface the store never shows. Full set and method: screens/README. The whole-set contact sheet is linked at the end.

The office / web side — the system of record

The web Portfolio Overview across all projects (RFI / submittal / financial status as red-amber-green bars per project) — the executive consumption surface. This is the office side that carries the platform’s value and that the App Store never shows.

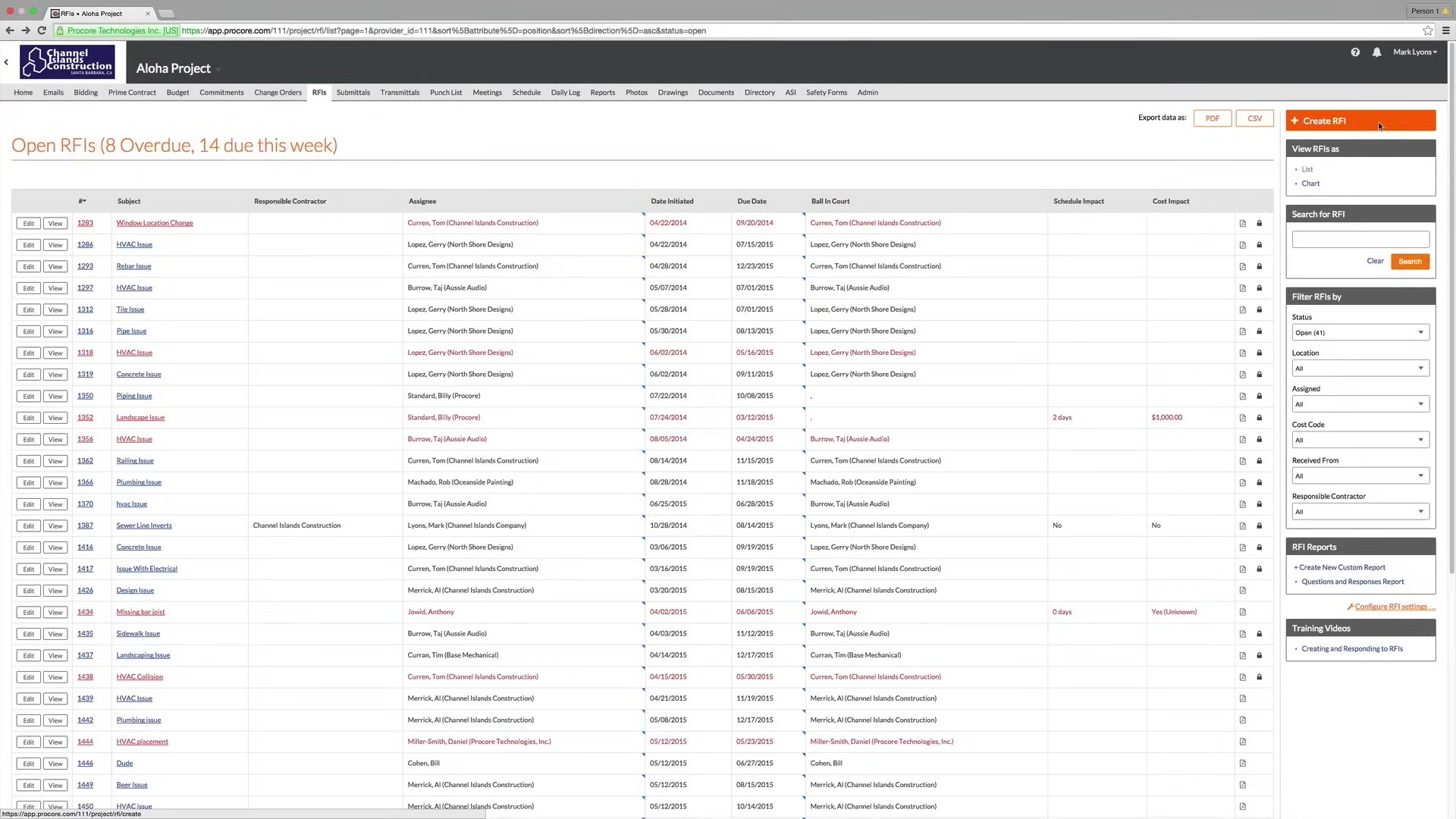

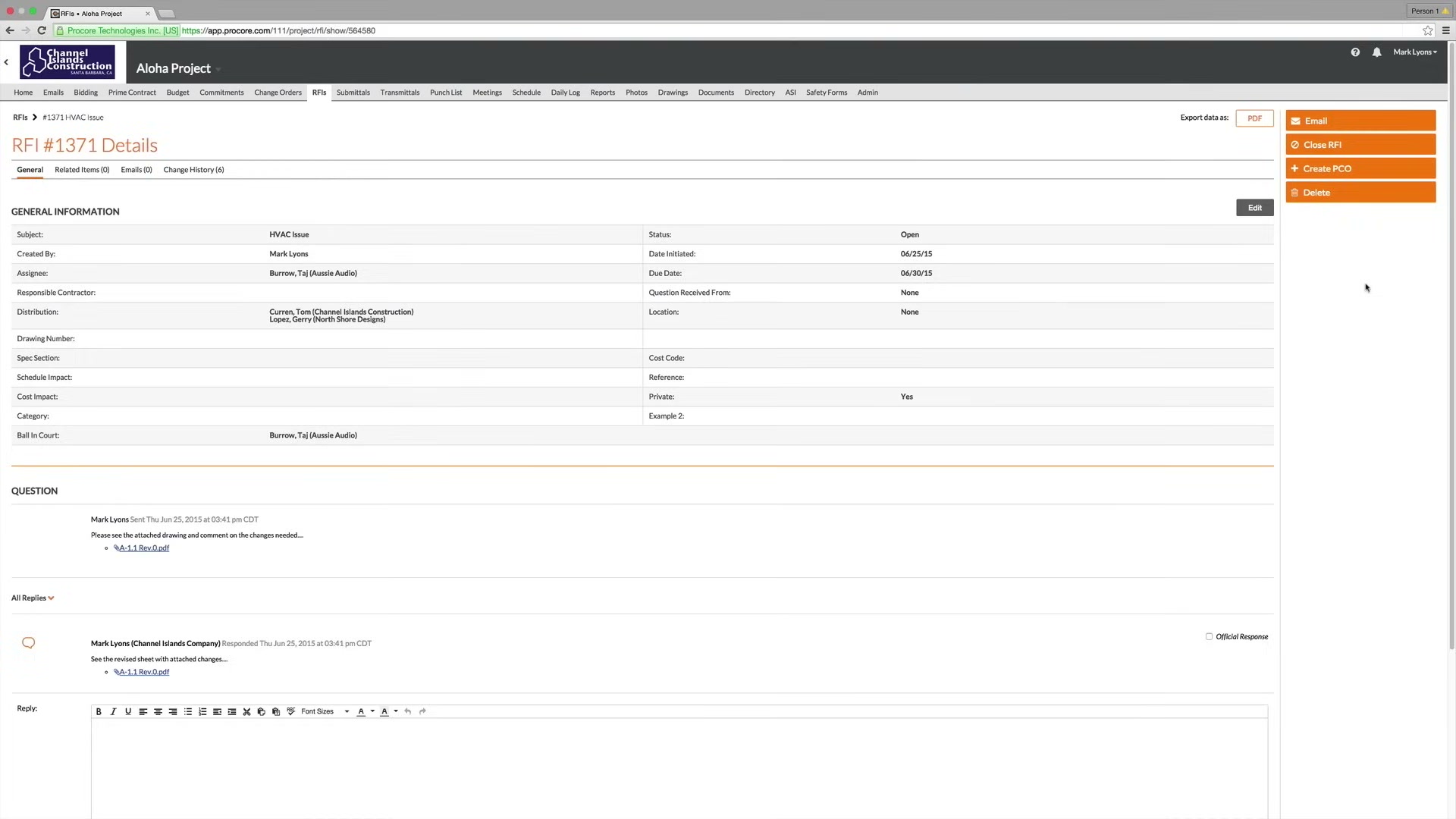

Document control — RFIs with commercial impact

The Open RFIs log for a project, with Schedule Impact and Cost Impact columns alongside responsible-contractor and ball-in-court — document control wired directly to the commercial record. This is Procore’s best-in-class core.

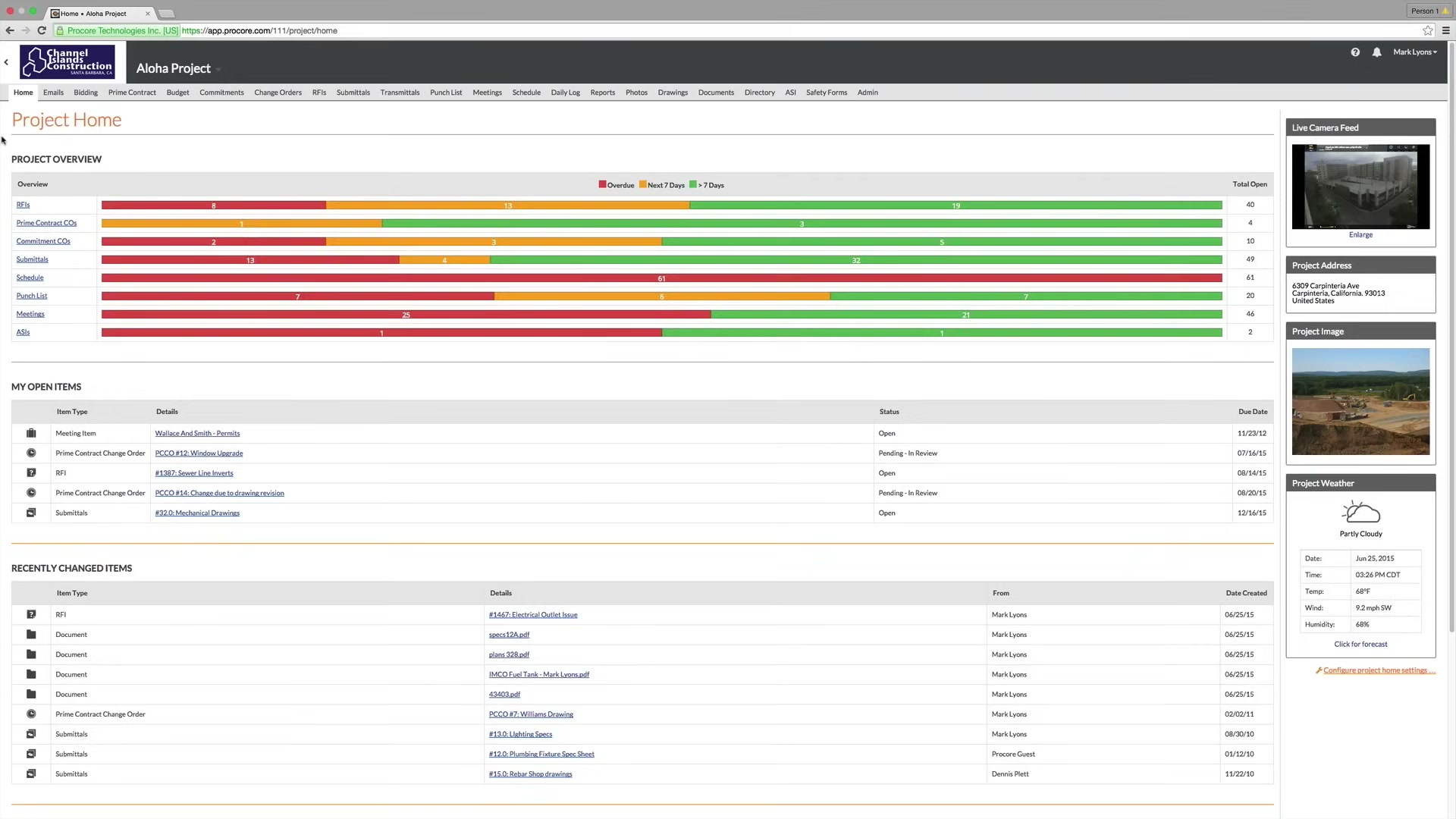

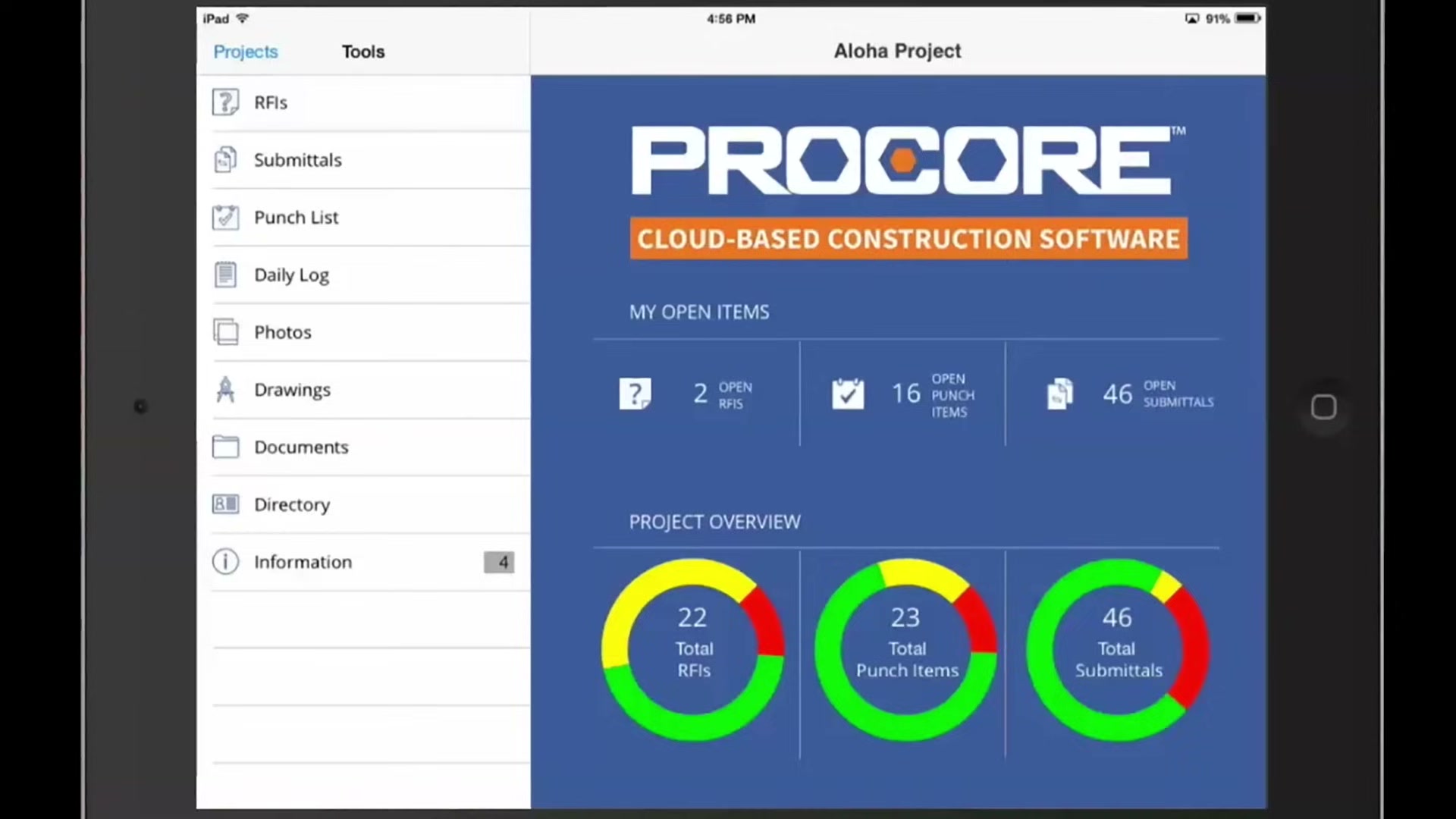

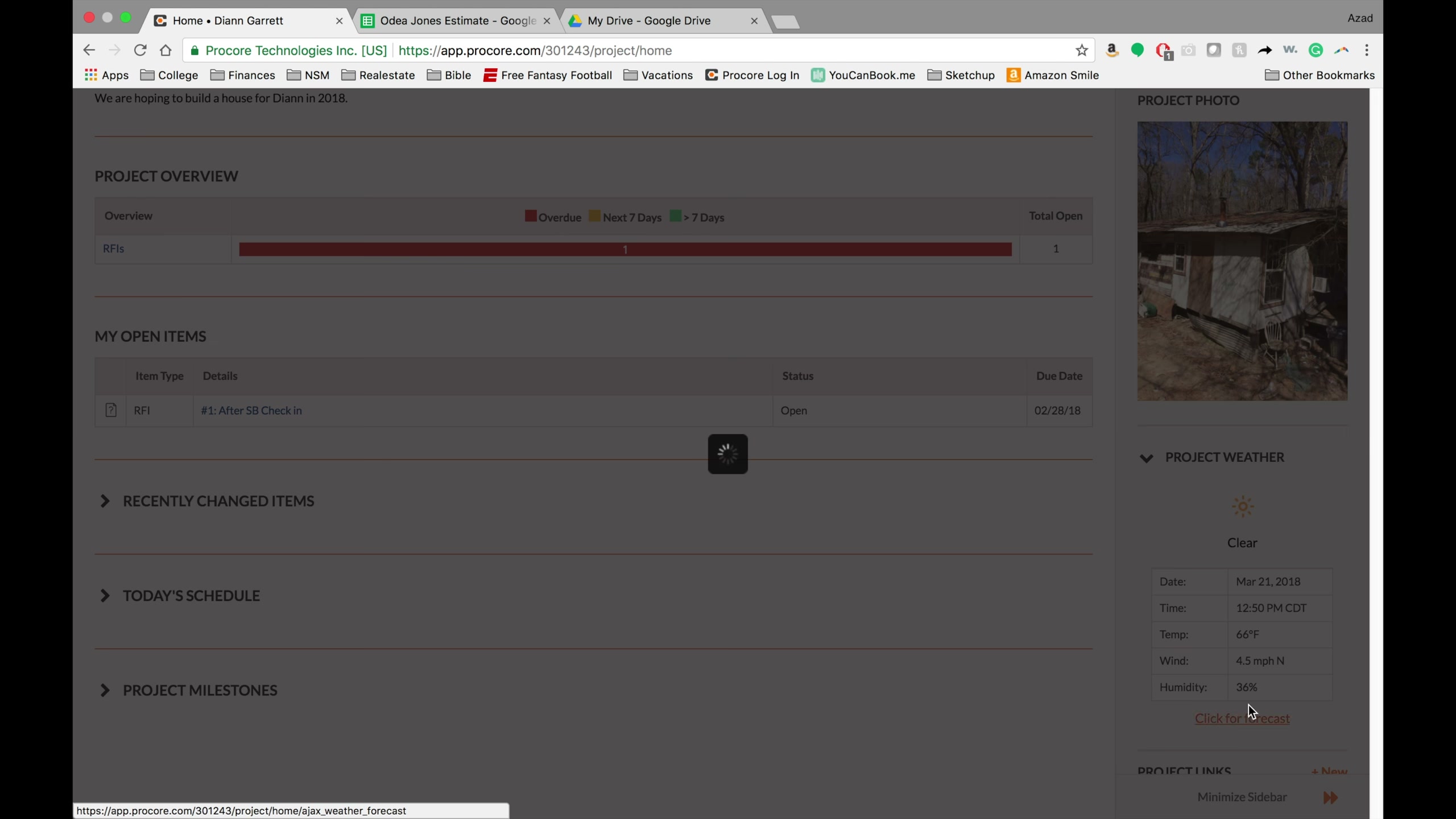

A single project — the daily picture

A per-project home: project overview with open-item rollups, my open items, today’s schedule, recent changes, and a live project-weather panel — the field-and-office daily view in one place.

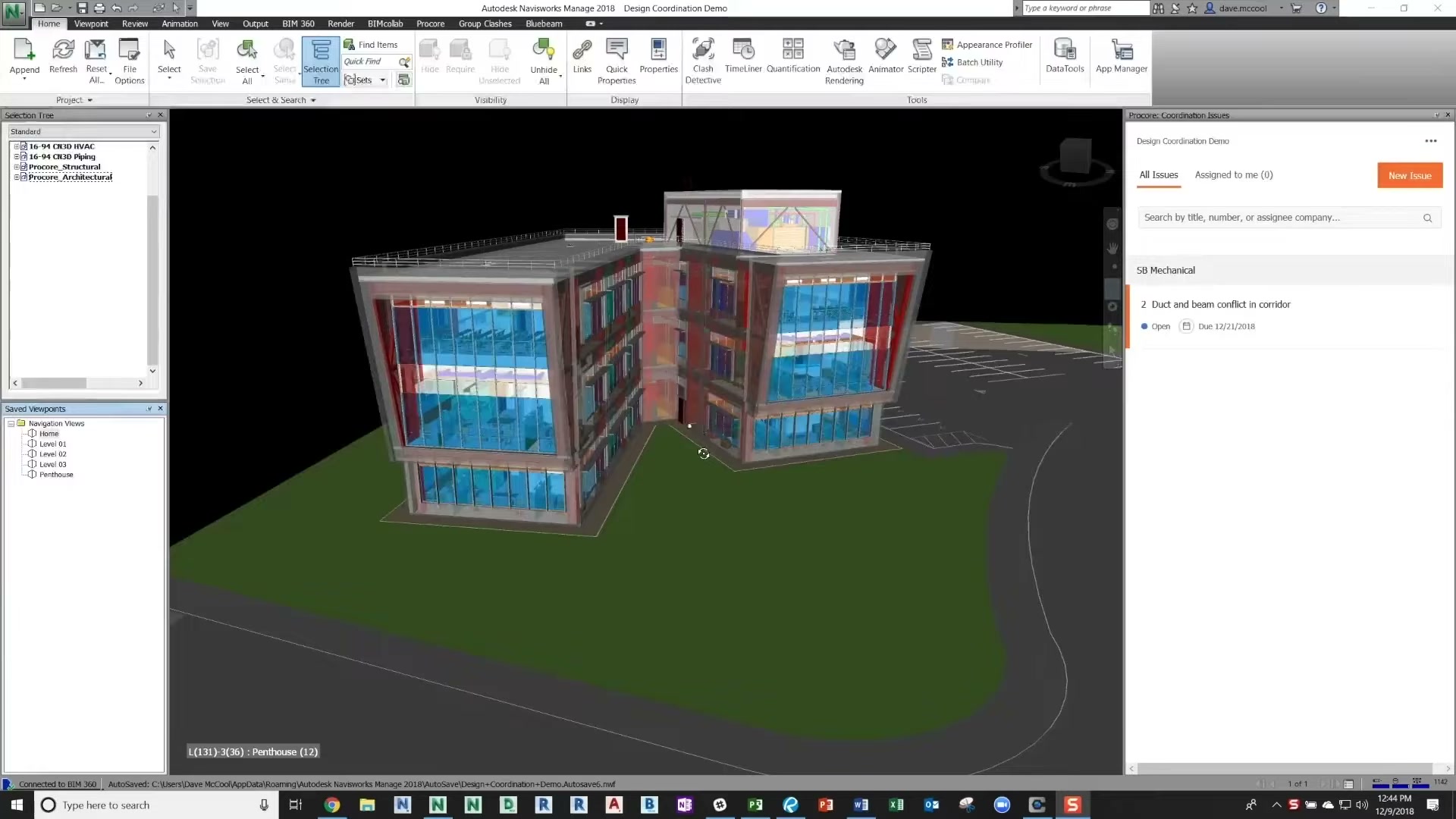

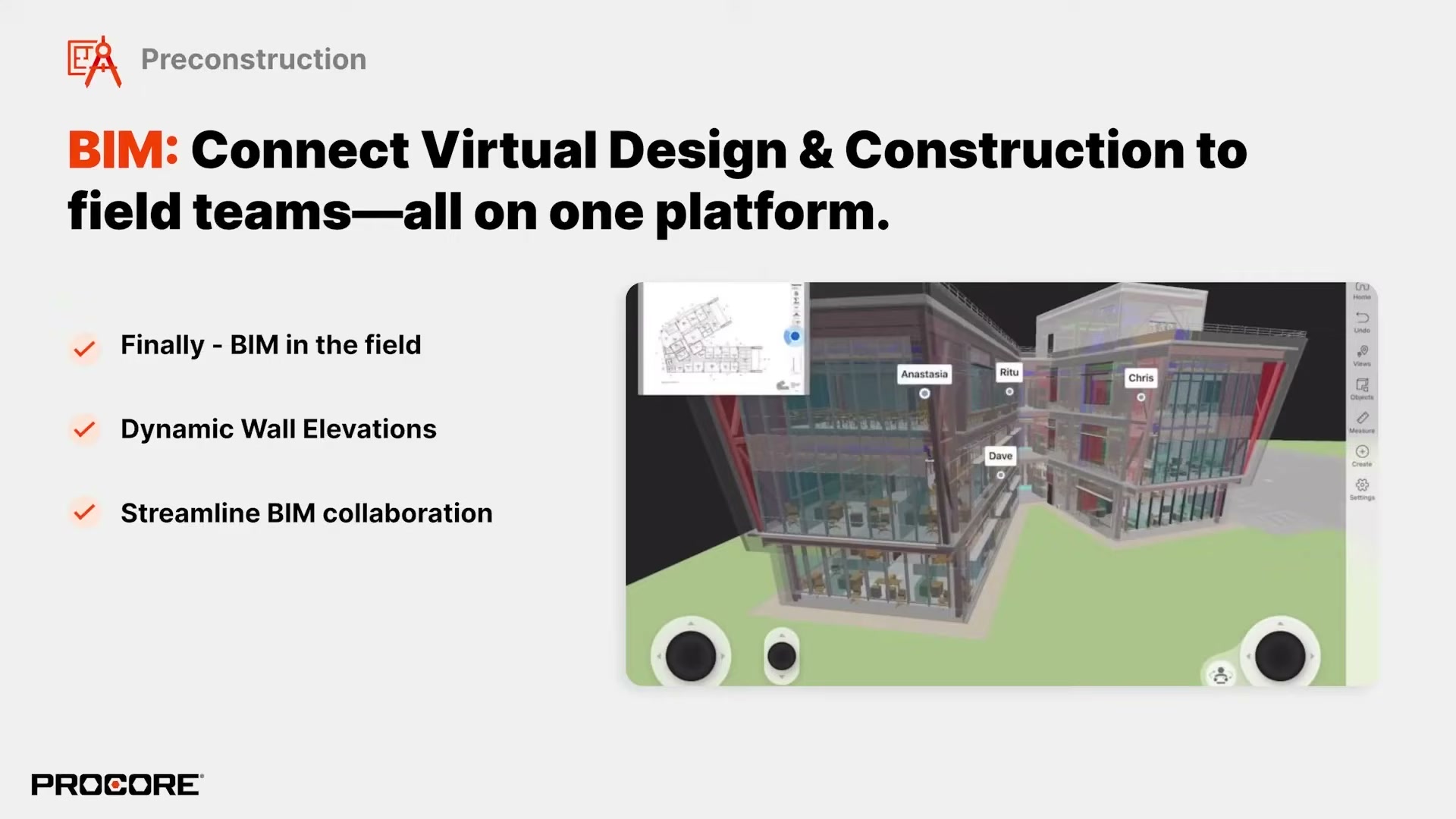

Preconstruction and BIM coordination

The preconstruction pitch (estimate, plan, predictability) shown against a 3D coordination model with a mobile coordination-issue card; and the model-coordination workflow itself (a duct-and-pipe clash opened as a coordination issue tied to the record).

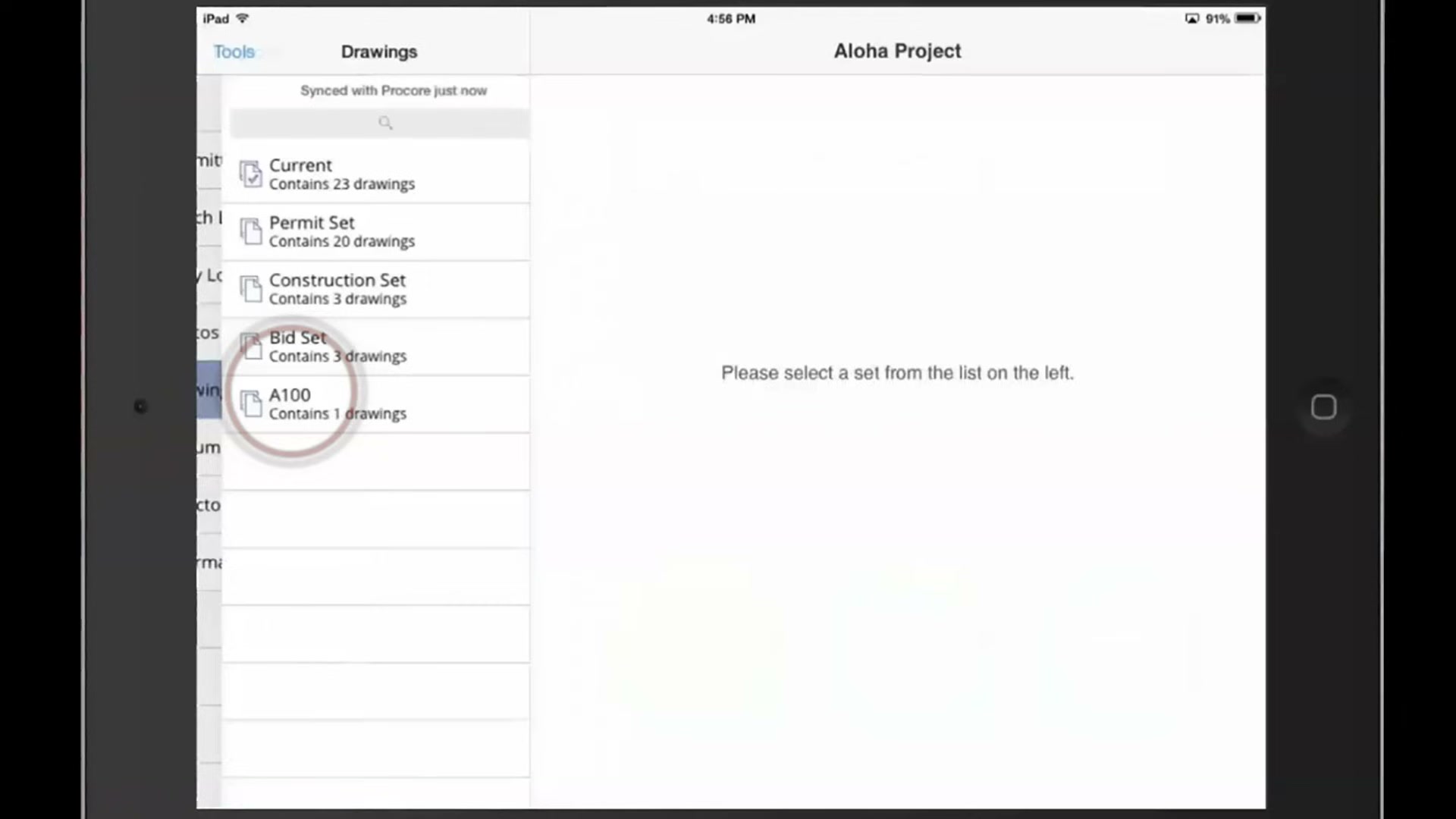

In the field — mobile drawings

The iPad app browsing synced drawing sets (Current, Permit Set, Construction Set, Bid Set) — the field front door to the same record the office works in.

Whole-set contact sheet

For a single-glance overview of everything captured from the walkthrough videos: contact_video.jpg (all frames — overview, platform, desktop, demo).

Sources and method

- Product surface / modules / personas: vendor platform page + App Store listing description (full module list: Field Enablement, Workforce Management, Project Management, Quality & Safety, Project Financials, Conversations open beta, Quick Capture) —

raw/appstore_app_us.json, plusprocore.com/platform. - Pricing model (ACV, not per-seat; unlimited users; quote-only; ~$15k-$75k+ range; ~$20M volume target):

procore.com/pricingcorroborated byraw/exa_answer.jsonandraw/exa_search.json. - App Marketplace + developer platform (REST API, OAuth2, webhooks, sandbox, MCP/agent components, 200-500+ integrations):

marketplace.procore.com,developers.procore.com, and search corroboration. - Procore’s own AI (Helix / Assist / Agent Builder / Datagrid acquisition / the May 21 2026 agent suite, with shipped-vs-beta status and dates): Procore press + investor releases and Groundbreak 2024/2025 coverage — captured in this brief’s AI table; the decisive primary sources are the Groundbreak 2025 “New AI Innovations” press release and the May 2026 “New Procore AI Experience Embeds Datagrid” investor release.

- Reviews (real segmentation): 100-review DOM/RSC sample (a four-page slice of ~2,645 Capterra reviews) recovering real firm-size, role, industry, sub-ratings and solicitation mix —

raw/capterra_dom_corpus.json, rolled up inraw/SUMMARY_DOM.md. Cross-checked against Capterra (~4.5/~2,645) and G2 (4.6/4,094). - App Store ratings:

raw/appstore_app_us.json,raw/appstore_app_gb.json. Screenshots and gathering method: screens/README. - Method, limits, and the discipline of not asserting an absence without evidence: _RESEARCH-METHOD.